Published by Sherry Cooper

September 16, 2024

Canadian Housing Market Stuck In A Holding Pattern

National home sales increased in June following the Bank of Canada’s first interest rate cut since 2020, and activity posted another slight gain in August on the heels of the second rate cut in late July. Still, the bigger picture appears to be a market mostly stuck in a holding pattern. Home sales recorded over Canadian MLS® Systems increased by 1.3% month-over-month in August 2024, reaching their highest level since January and their second highest in over a year.

“Despite some fledgling signs of life to kick off the long-awaited monetary policy easing cycle, Canadian housing market activity still looks to be stuck in the same holding pattern it’s been in all year,” said Shaun Cathcart, CREA’s Senior Economist. “That said, with ever more friendly interest rates now all but guaranteed later this year and into 2025, it makes sense that prospective buyers might continue to hold off for improved affordability, especially since prices are still well-behaved in most of the country.”

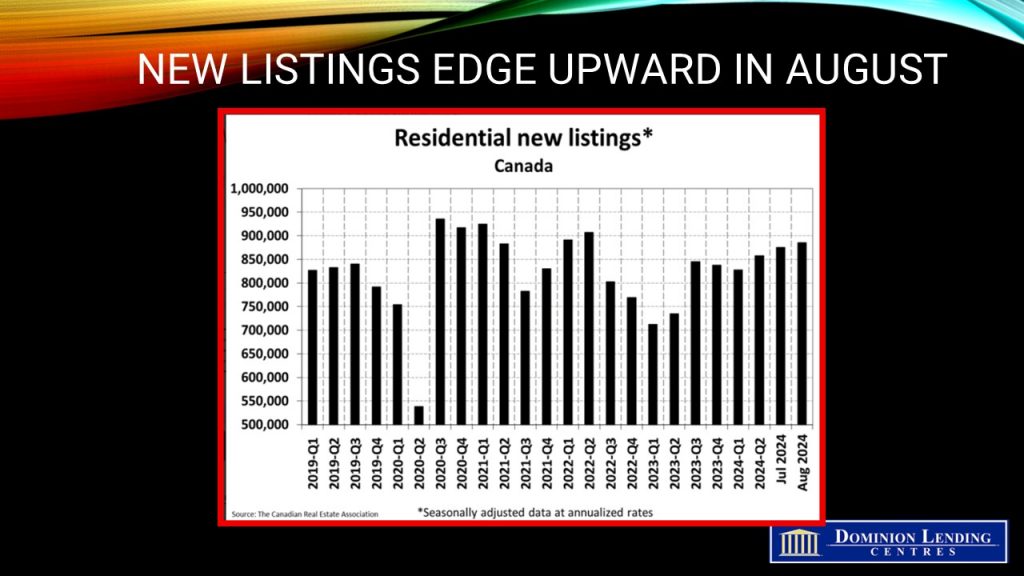

At the end of August 2024, about 177,450 properties were listed for sale on all Canadian MLS® Systems, up 18.8% from a year earlier but still more than 10% below historical averages of around 200,000 listings for this time of the year.

New Listings

As of the end of July 2024, about 183,450 properties were listed for sale on all Canadian MLS® Systems, up 22.7% from a year earlier but still about 10% below historical averages of more than 200,000 for this time of the year.

New listings posted a slight 0.9% month-over-month increase in July. A much-needed boost in new supply in Calgary led to the national increase in new supply in Calgary.

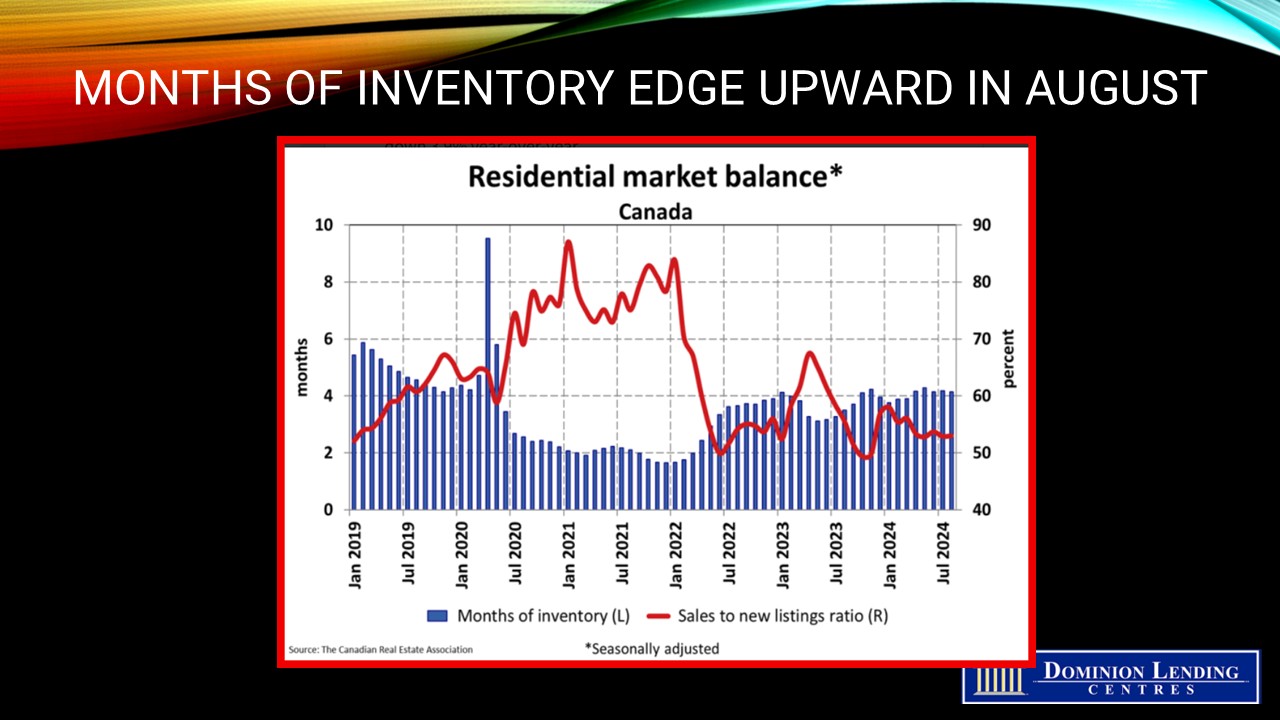

With new listings up slightly and sales down slightly in July, the national sales-to-new listings ratio fell to 52.7% compared to 53.5% in June. The long-term average for the national sales-to-new listings ratio is 55%, with a ratio between 45% and 65% generally consistent with balanced housing market conditions.

At the end of July, there were 4.2 months of inventory nationwide, unchanged from the end of June. The long-term average is about five months of inventory.

“While it wasn’t apparent in the July housing data from across Canada, the stage is increasingly being set for the return of a more active housing market,” said James Mabey, Chair of CREA. “At this point, many markets have a healthier amount of choice for buyers than has been the case in recent years, but the days of the slower and more relaxed house hunting experience may be somewhat numbered.

At the end of August 2024, there were 4.1 months of inventory on a national basis, down from 4.2 months at the end of July. Continuing the theme of the market being in a holding pattern, this measure of market balance has been range-bound between 3.8 months and 4.2 months since last October. The long-term average is about five months of inventory.

{kind=link}

{kind=link}

Home Prices

The National Composite MLS® Home Price Index (HPI) increased by 0.2% from June to July. While a slight increase, it was slightly larger than the June increase, making it just the second and the most significant gain in the last year.

While prices were up slightly at the national level, they were held back by reduced activity in the most extensive and expensive British Columbia and Ontario markets. Regionally, prices are rising in most markets.

The non-seasonally adjusted National Composite MLS® HPI stood 3.9% below July 2023. This primarily reflects how prices took off last April, May, June, and July—something that was not repeated over that same period in 2024. Year-over-year comparisons will likely improve from this point on.

The actual (not seasonally adjusted) national average home price was $667,317 in July 2024, almost unchanged (-0.2%) from July 2023.

The National Composite MLS® Home Price Index (HPI) was unchanged from July to August, following two small increases in June and July. That said, the bigger picture is that prices at the national level have been flat since the beginning of the year, posing no reason for potential buyers to rush to market.

The non-seasonally adjusted National Composite MLS® HPI stood 3.9% below August 2023. This mostly reflects price gains last spring and summer, followed by declines in the second half of last year. As such, it’s mostly likely that year-over-year comparisons will improve from this point on.

Bottom Line

Potential homebuyers remain on the sidelines awaiting further rate cuts by the Bank of Canada. As long as home prices are flat, purchasers have no compelling reason to take immediate action. This should change gradually. With new supply on the market, sales should continue to rise this month.

With weak labour markets and falling economic growth, the Bank of Canada will continue to cut interest rates by at least 25 bps on each decision date. Governor Macklem has commented that more significant rate cuts would be forthcoming if the economy weakens too aggressively and inflation falls below the 2% target. This would be welcome news for housing. We expect the overnight policy rate to fall to 2.5% before the end of next year. It is now at 4.25%–well above the current inflation rate.

In separate news, the Trudeau government has taken action to implement some of the budget measures to improve housing affordability. The federal government will make 30-year mortgages available to all first-time buyers and to buyers of newly built homes.

Canada cracked down on lengthy mortgage amortizations during the 2008 global financial crisis. Until this year, buyers who required government-backed default insurance on their mortgages were limited to 25-year amortizations.

Trudeau and Finance Minister Freeland stepped toward loosening that rule in April, allowing 30-year amortizations on insured mortgages only for first-time buyers purchasing newly built homes.

The government will also begin allowing mortgage default insurance on homes worth up to $1.5 million, an increase from the current cap of $1 million, effective December 15. That means buyers can bid on more expensive homes even if they have less than a 20% down payment — as long as they purchase insurance.

Today’s announcement will significantly expand the pool of buyers who can access 30-year loans, which lowers monthly payments. According to Freeland, insured first-time buyers represent roughly 20% of the market in Canada, while new builds make up about 4%.

Please Note: The source of this article is from SherryCooper.com/category/articles/