By Leanne Mollica

Mortgage Broker | Mortgage Architects – Team Borle

Founder, My Mortgage Strategy

Serving Salmon Arm, the Shuswap, and British Columbia

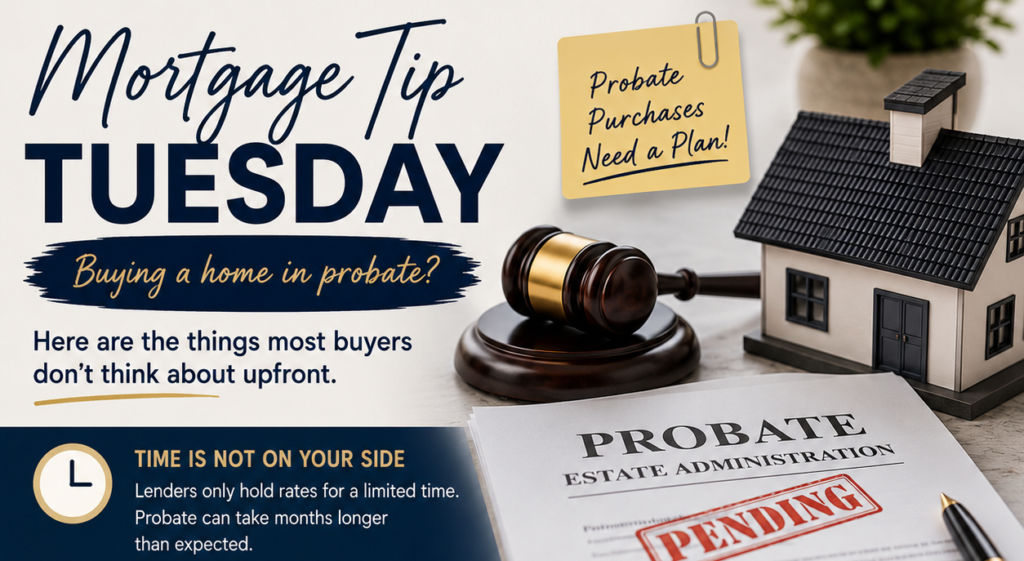

Probate purchases can create some very unique mortgage and financing challenges that most buyers do not think about upfront.

On paper, these transactions can seem fairly straightforward.

You find the perfect home.

Your offer gets accepted.

Your mortgage gets approved.

Everything appears to be moving forward normally.

Except there is one major complication:

The estate is still waiting for probate.

And this is often the exact moment a mortgage broker’s anxiety spikes.

The Court Timeline and the Mortgage Timeline Are Not the Same Thing

One of the biggest issues with probate purchases is timing.

Many buyers assume that once financing is approved, everything else will simply fall into place. Unfortunately, probate timelines can be extremely unpredictable.

While some estates move through the court process relatively quickly, others can experience delays that stretch for months.

The problem?

Mortgage approvals and rate holds are not indefinite.

Most lenders only hold an interest rate for a limited period of time. In many cases, buyers may only have a 90- to 120-day rate hold.

That means if probate drags on too long:

- the original interest rate may expire,

- the borrower may need to requalify,

- updated documents may be required,

- and the file may need to be re-underwritten entirely.

In a rising rate environment, this can become very expensive very quickly.

I am currently working on probate files where buyers have already moved into the property under occupancy agreements while still waiting for probate to complete — all while watching the clock count down on their remaining rate hold.

That creates real financial pressure.

Occupying the Property Before Completion Can Create Major Issues

This is another area where probate transactions become much more complicated than buyers expect.

Often, the estate and the buyer attempt to solve probate delays by allowing the buyer to move into the property before legal completion through:

- occupancy agreements,

- temporary rental arrangements,

- or “move in early” arrangements while probate is finalized.

At first glance, this can seem harmless.

But from a lender and insurer perspective, the moment someone occupies the property before closing, several major risk questions immediately arise.

Questions like:

- Is this effectively becoming a rent-to-own arrangement?

- Has beneficial ownership already transferred before closing?

- Who carries liability if something happens to the property before title transfers?

- Is the occupancy agreement properly structured legally?

- Could this arrangement impact the enforceability of the mortgage?

What sounds like a simple solution can quickly become a legal, insurance, and financing headache if it is not carefully structured.

This is especially important for insured mortgages, where the mortgage insurer may scrutinize occupancy arrangements very carefully.

Probate Purchases Often Require More Strategy

One of the biggest misconceptions in mortgage financing is that approvals are only about:

- income,

- credit score,

- and down payment.

Those things absolutely matter.

But unusual transactions — including probate purchases — often introduce legal and structural concerns that can become the biggest obstacle in the file.

Sometimes the borrower qualifies perfectly.

The property qualifies.

The down payment is solid.

But the timing and structure of the transaction create complications that require careful planning.

What Buyers Should Do Before Removing Subjects

If you are considering purchasing a home that is still in probate, it is extremely important to involve your mortgage broker early and ensure everyone understands:

- the probate status,

- estimated timelines,

- occupancy plans,

- rate hold expiries,

- and any proposed early possession arrangements.

The earlier these issues are identified, the more options there typically are to structure the transaction properly.

Because sometimes the hardest part of getting a mortgage is not income, credit, or down payment.

Sometimes the legal structure and timing of the transaction become the biggest challenge.

And that is exactly why unusual transactions require proper upfront planning before subjects are removed.

Leanne Mollica is a Mortgage Broker with Mortgage Architects – Team Borle, serving Salmon Arm, the Shuswap, and clients across British Columbia. Through My Mortgage Strategy, she helps borrowers navigate everything from standard purchases to complex and unusual financing scenarios with proactive planning and honest guidance.