By Leanne Mollica

Mortgage Broker | Mortgage Architects – Team Borle

Founder, My Mortgage Strategy

Serving Salmon Arm, the Shuswap, and British Columbia

This morning’s theme in my inbox was clear:

“Should I lock in my variable rate?”

If you currently have a variable-rate mortgage, this post is for you.

Let’s break down what’s going on in the mortgage world right now — in plain English.

The Ride Variable Mortgage Holders Have Been On

Many homeowners who took a variable mortgage recently have only experienced rates going down.

And honestly… that’s been a pretty nice ride.

But this week the tone from the Bank of Canada shifted slightly, and it’s something worth understanding if you’re in a variable rate.

This doesn’t mean rates are about to jump tomorrow.

But it does mean the road ahead may not be a straight line downward like it has been recently.

Why the Bank of Canada Raises Rates

Many people assume rates only rise when the economy is overheating from too much spending.

But inflation can come from many different sources, including:

- Global conflicts or geopolitical tensions

- Rising energy prices

- Supply chain disruptions

- Tariffs or international trade changes

- Extreme weather impacting food supply

When these types of pressures push prices higher, the Bank of Canada may raise rates to keep inflation under control.

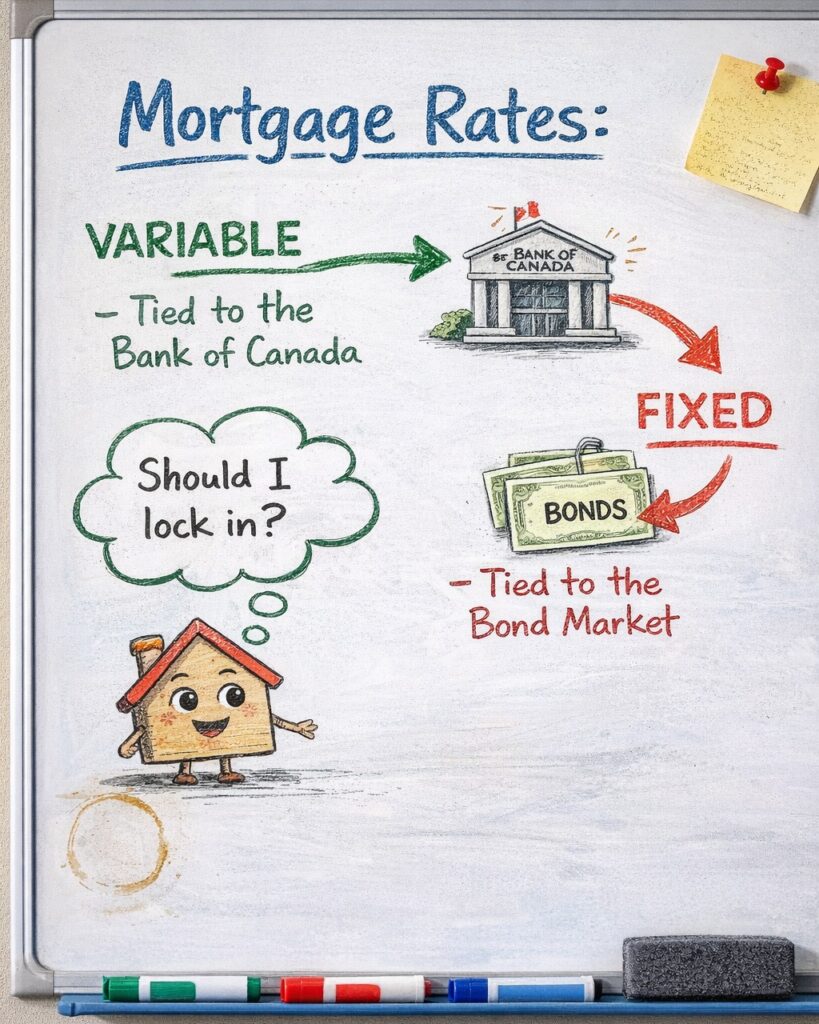

The Important Difference Between Variable and Fixed Rates

This is one of the most misunderstood parts of mortgages.

Variable Rates

Variable rates move directly with the Bank of Canada’s policy rate.

If the Bank cuts rates → variable rates fall.

If the Bank raises rates → variable rates rise.

Fixed Rates

Fixed mortgage rates do not move with the Bank of Canada.

They are driven by bond markets, specifically Government of Canada bond yields.

Bond markets react very quickly to global events and investor sentiment.

If investors begin worrying about future inflation, bond yields rise — and fixed mortgage rates often rise with them.

This means:

The fixed rate your lender offers today could look very different in a few months.

Should You Lock In Your Variable Mortgage?

The answer isn’t the same for everyone.

But if you currently have a variable mortgage, one simple step can give you clarity:

Call your lender and ask what fixed rate they would offer if you locked in today.

Most variable mortgages allow you to convert to a fixed rate without penalty.

Important:

You are not committing to anything by asking.

You’re simply gathering information.

Sometimes the Best Decision Is Just Understanding Your Options

In some situations, staying variable still makes perfect sense.

In other cases, locking into a fixed rate helps people sleep better at night.

There is no universal answer.

The right choice depends on:

- Your comfort with risk

- Your household budget

- Your long-term plans

- Your personal stress tolerance

And sometimes, the biggest benefit is simply knowing your options ahead of time instead of reacting later.

Want a Second Opinion?

If you want help reviewing your options, feel free to send the numbers my way.

I’m always happy to take a look and help you compare scenarios so you can make the decision that feels right for your household.

At the end of the day, my job isn’t to tell you what to do.

My job is to make sure you understand the strategy behind the decision.