By Leanne Mollica

Mortgage Broker | Mortgage Architects – Team Borle

Founder, My Mortgage Strategy

Serving Salmon Arm, the Shuswap, and British Columbia

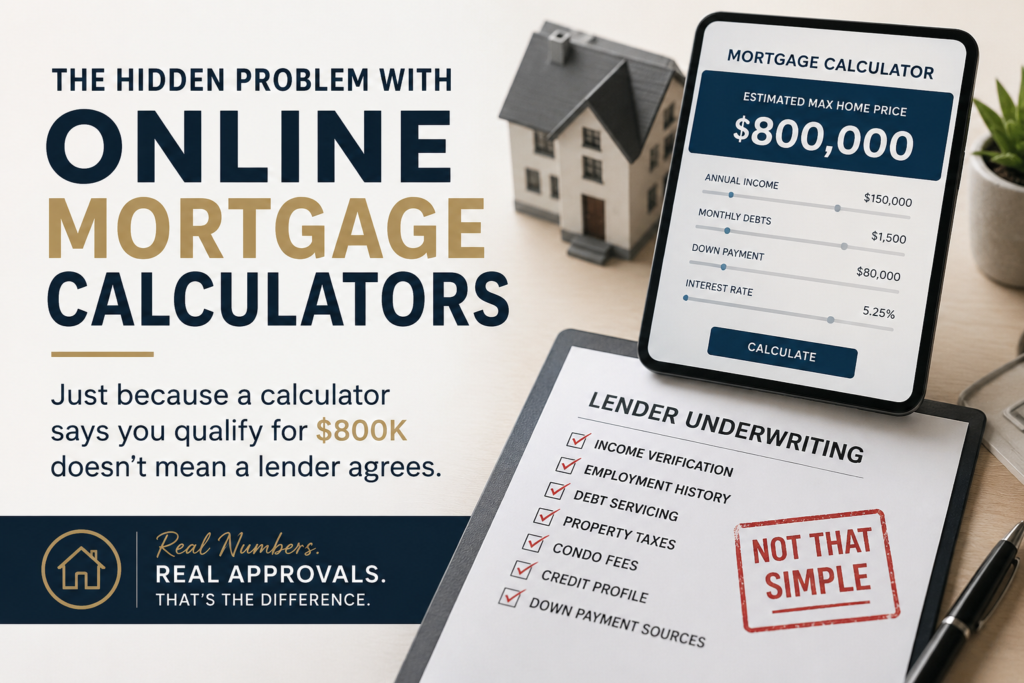

“According to the calculator, we qualify for $850,000.”

I hear this all the time.

And unfortunately… sometimes the lender disagrees.

Online mortgage calculators can be a great starting point, but they are exactly that — a starting point. Most calculators use very simplified math and don’t account for the dozens of factors lenders actually look at when approving a mortgage.

That’s where buyers can get blindsided.

Because on paper, the numbers might look fine. But once the file reaches underwriting, the story can change quickly.

Here are just a few things online calculators often miss:

Income Isn’t Always Calculated at Face Value

A buyer may earn:

- bonuses

- overtime

- seasonal income

- self-employment income

- commissions

- multiple jobs

But lenders don’t always use 100% of that income.

Some require a two-year average.

Some only use guaranteed hours.

Some exclude income completely if history is too short.

So while a calculator may say someone qualifies for an $800,000 purchase, the lender may only recognize part of the income that got them there.

Property Taxes & Condo Fees Matter More Than People Think

Debt servicing ratios are one of the biggest factors in mortgage qualification.

That means:

- higher property taxes

- condo fees

- heating costs

- monthly debts

…all directly impact purchasing power.

I’ve seen buyers qualify comfortably on one property and not qualify at all on another with the exact same purchase price simply because the carrying costs were different.

“Pre-Approved” Doesn’t Always Mean Underwritten

This one surprises people the most.

A lot of lender pre-approvals are based primarily on:

- credit

- application information

- automated systems

Sometimes no income documents have been reviewed yet at all.

That’s why buyers can feel confident right up until financing conditions — and then suddenly run into problems when the actual documents are reviewed.

This Is Why My Process Is Different

I’m a big believer in finding problems before an offer is written — not after.

That’s why I review documents upfront, calculate income the way lenders actually do, and pressure-test files early.

Does that mean a little more homework for buyers at the beginning?

Absolutely.

But it also means clients can shop with confidence knowing the numbers have actually been reviewed — not just estimated by a calculator or automated system.

Because in today’s market, strategy matters.

But accuracy matters too.