Published by Sherry Cooper

June 27, 2025

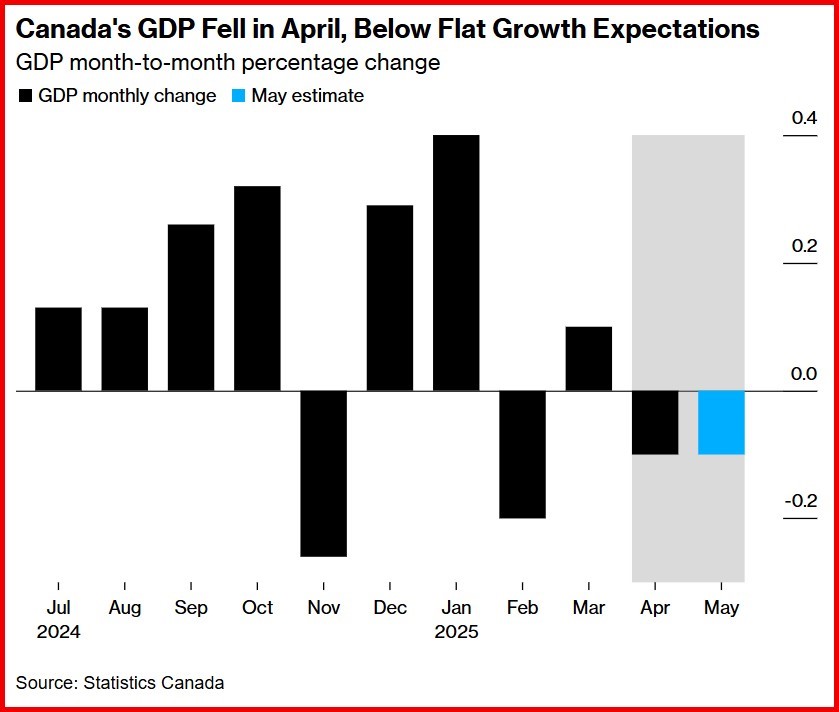

Canada Is Headed For A Moderate Economic Contraction in Q2

Real gross domestic product (GDP) edged down 0.1% in April, following a 0.2% increase in March. The preliminary estimate for May was also -0.1%.

April and May were months of the most significant tariff uncertainty–both auto, steel, and aluminum tariffs were announced during this period. The 0.1% drawdown in April GDP had a wide variety of special factors at play in that month of high drama. The biggest drag by far was a steep 1.9% fall in manufacturing, including a 5.2% drop in the auto sector, as firms dealt with the initial wave of tariffs, as well as some further pullback after earlier tariff front-running.

Tariff front-running led to a surge in US imports in the first quarter. Revisions to the Q1 data in the States now show a 0.5% contraction, worse than initially reported.

Other trade-related sectors were soft, with wholesale trade down 1.9% and transportation & warehousing off 0.2%. Providing some offset was the Federal election in the month, which boosted federal public administration 2.8% m/m. StatCan notes that the start of the NHL playoffs, with five Canadian teams in the mix (more than usual), boosted the arts and entertainment sector by 2.8%. Hotels and restaurants also firmed (+0.6%), potentially supported by Canadians vacationing closer to home, and the NHL playoffs may have also contributed to the increase. Were it not for the election boost and entertainment, real GDP would have been down 0.2% in April.

May’s expected drop was due, in part, to the reversal of the election bump in public administration spending, as well as softness in the resource sector and retail trade. Notably, StatCan did not mention manufacturing as a source of weakness. Still, earlier this week, it reported a 1.3% drop in May factory sales and a 0.4% decline in wholesale in flash reports, which no doubt also weighed.

{kind=link}

In other news, the US released its May personal consumption expenditures, which fell 0.3% after adjusting for inflation. President Trump’s economic policies are weighing on the outlook for US growth, which could prompt the Fed to take action in the coming months.

The Federal Reserve’s preferred inflation gauge, the PCE price index minus food and energy, rose 0.2% — slightly more than expected, though still consistent with limited price pressures.

The decline in spending, which was broad-based, coincides with depressed consumer sentiment this year in response to President Donald Trump’s unpredictable trade policy. Inflation has been muted so far in 2025, although many economists expect it to pick up in the next few months as businesses increasingly pass higher import duties on to households.

The latest figures suggest sluggish US household demand, especially for services, extended into May after the weakest quarter for personal consumption since the onset of the pandemic. Spending on transportation services, meals out, accommodation, financial services, and other services — a category that includes net foreign travel — all declined last month. US personal income, meanwhile, fell in May by the most since 2021 on a pullback in government transfers, led by a decrease in Social Security payments. The saving rate fell to 4.5%.

Bottom Line

Chair Jay Powell told Congress this week that he expects inflation to pick up in June, July and August as tariffs become increasingly reflected in consumer prices. However, he added that if that prediction fails to materialize, the US central bank could resume interest-rate reductions sooner rather than later.

Weaker consumer and business spending, along with modest inflation, bode well for another rate cut by the Bank of Canada as well. Many economists now believe the Bank’s rate-cutting cycle is over.Many economists now believe the Bank’s rate-cutting cycle is over. I’m not convinced.

Please Note: The source of this article is from SherryCooper.com/category/articles/